Finding the Best Homeowners Insurance in Florida

Homeowners insurance in Florida costs significantly more than the national average, with premiums running 50–80% higher due to hurricane exposure and weather risk. At Responsive Insurance, Inc., we help Naples residents navigate these higher costs and find the best homeowners insurance in Florida that actually fits their budget.

Your lender requires specific coverage, major carriers have pulled out of the state, and your options feel limited. This guide walks you through what makes Florida insurance different and how to compare quotes effectively.

Why Florida Homeowners Pay So Much More

Hurricane Risk Drives Premiums Skyward

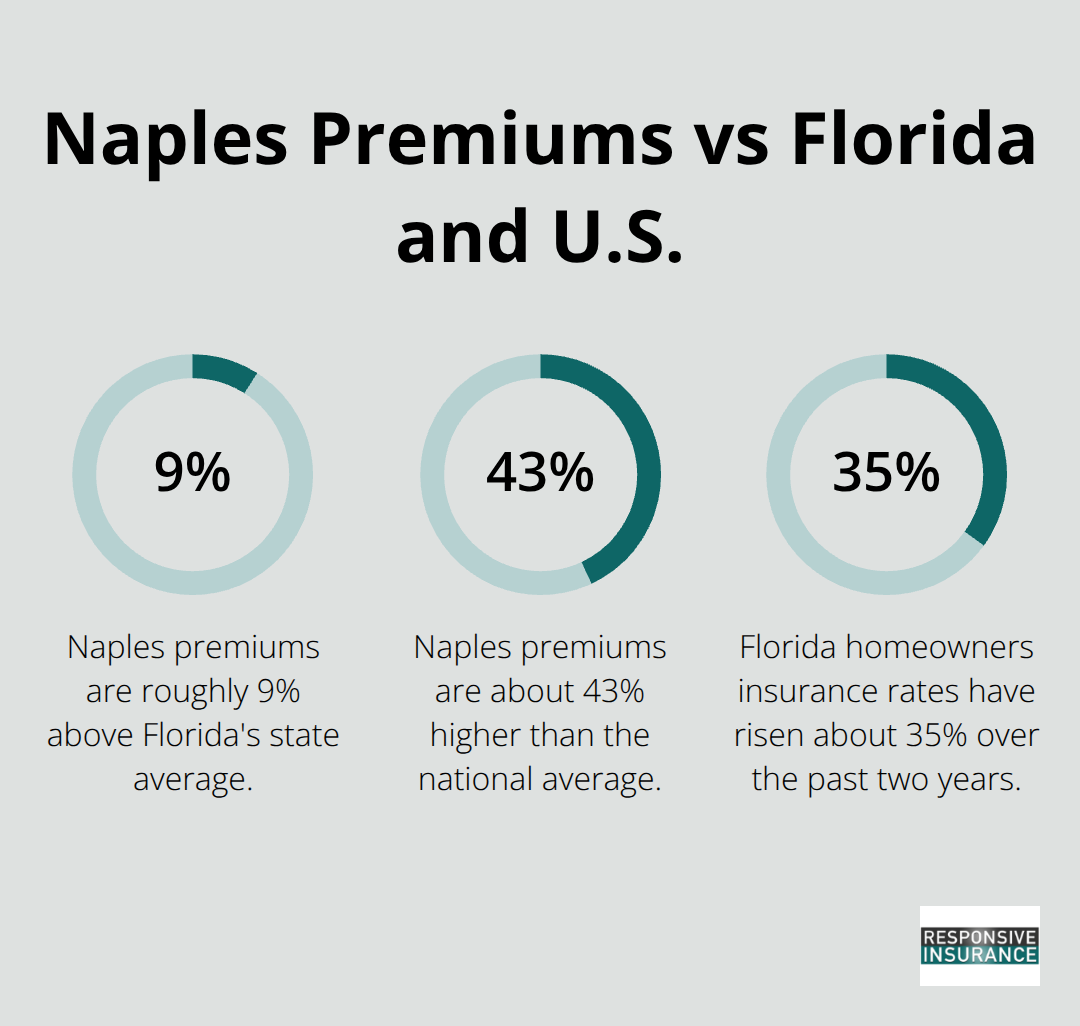

Florida homeowners face insurance costs that dwarf the national average. Naples homeowners pay around $2,502 per year, roughly 9% above Florida’s state average and 43% above what Americans pay nationally. This gap exists for one reason: hurricanes. Over the past two years, Florida homeowners insurance rates have risen about 35% on average due to the high frequency of destructive hurricanes and expensive claim losses.

When a major storm hits, insurers don’t absorb those costs quietly-they pass them directly to policyholders through higher premiums across the state.

Coverage Levels and Deductibles Shape Your Bill

The financial burden doesn’t stop at base rates. If you want $500,000 in dwelling coverage on a Naples home, you’ll pay around $4,193 per year, which shows how coverage level drives cost upward. Raising your deductible from $500 to $1,000 can save roughly $1,000 annually, but that trade-off means you absorb more risk yourself after a claim. What matters most is understanding that Florida’s risk profile has fundamentally changed the insurance market.

Lenders Mandate Coverage You Cannot Avoid

Lenders won’t approve a mortgage without proof of homeowners insurance, and they require specific coverage minimums tied to your home’s value. This mandatory requirement gives you no choice but to carry insurance, even when prices feel unreasonable. The real problem compounds when you discover that major national carriers have drastically reduced their presence in Florida or exited entirely.

Limited Carrier Options Force Difficult Choices

State Farm remains available in Naples with competitive rates averaging around $2,016 per year and AM Best A++ financial strength ratings, but other big names have simply walked away. Citizens Insurance exists as a high-risk, last-resort option at around $6,281 per year-roughly 2.5 times the State Farm average. This limited competition means fewer options to negotiate rates or find better terms.

Smaller, regional carriers like Tower Hill, Universal Property, and Security First fill some gaps, but their financial strength ratings vary, and customer complaint histories differ significantly. Tower Hill recorded notably higher complaint levels compared with similar-sized insurers in 2022, while Universal Property carries roughly 11 times more complaints than comparable companies. Shopping around becomes essential not because you want to, but because you have to. The carriers available today differ wildly in price, reliability, and financial stability. As an independent agency based in Naples, Responsive Insurance, Inc. works with multiple A-rated insurance companies to compare coverage and find the best fit for your needs. Direct comparison remains the only way to protect yourself and identify which carrier aligns with your budget and risk tolerance.

What Coverage Actually Matters for Your Naples Home

Comparing homeowners insurance quotes means understanding what each dollar of premium buys you, and this becomes critical in Florida where coverage gaps cost you thousands after a hurricane. The three areas that separate a worthwhile policy from a dangerous gap are dwelling coverage limits, deductible choices, and specialized protections for flood and wind damage. Most Naples homeowners focus only on the lowest premium without realizing they’ve purchased inadequate coverage or missed essential protections entirely. We see this mistake repeatedly, and it costs families dearly when storms hit.

Dwelling Coverage and Deductibles Set Your Real Cost

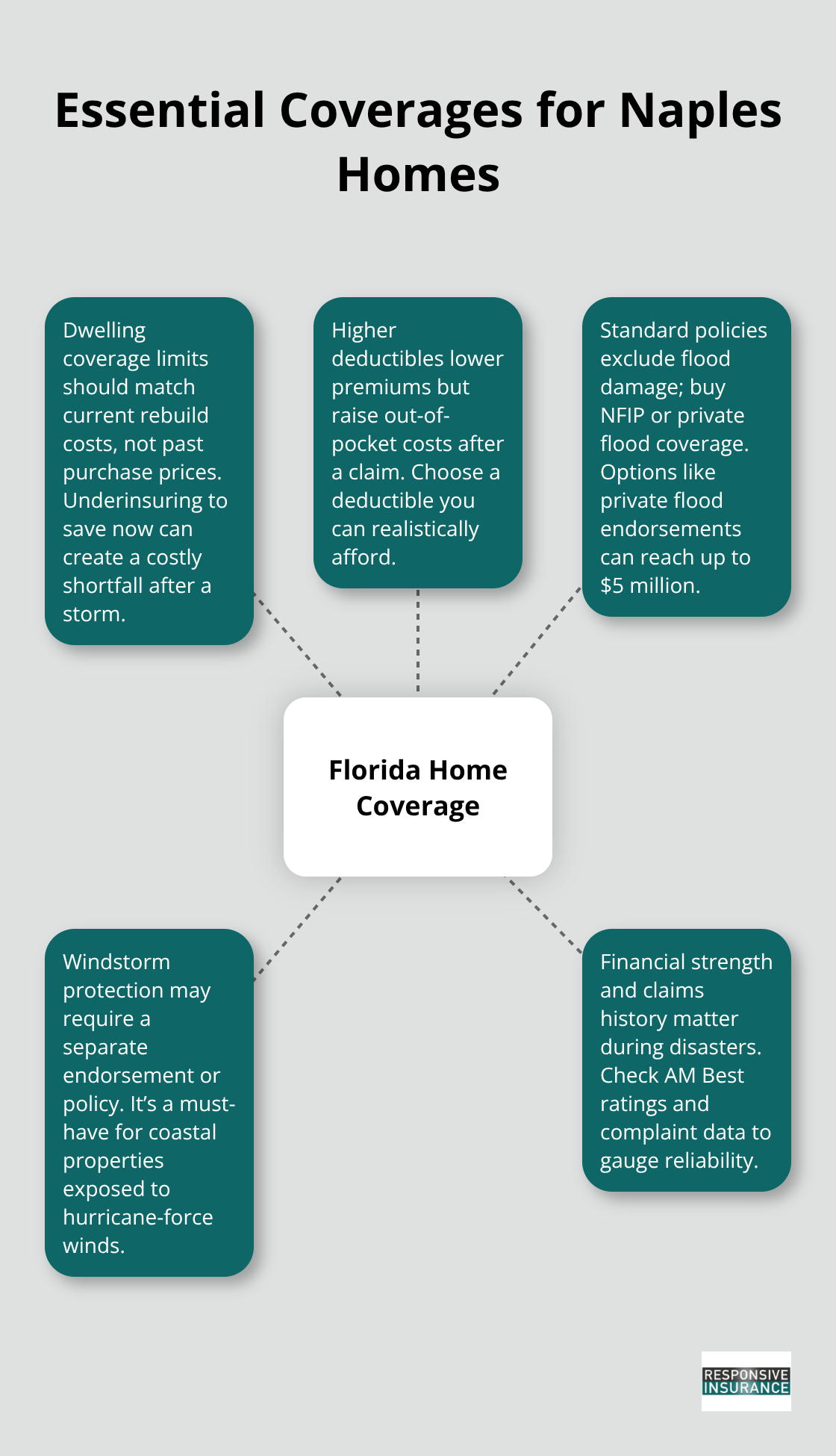

Your dwelling coverage limit determines how much your insurer will spend to rebuild if your home is destroyed, and this number must reflect current construction costs, not what your home sold for five years ago. A Naples homeowner with $500,000 in dwelling coverage pays around $4,193 per year, while someone with a lower limit might pay $2,502 annually-illustrating how coverage selection directly impacts your bill. The mistake happens when homeowners choose a lower limit to save money upfront, then face a shortfall if rebuilding becomes necessary. Construction inflation in Florida means rebuild costs exceed pre-storm market values, so your coverage limit should reflect what it actually costs to rebuild, not your home’s purchase price.

Your deductible works the opposite way: higher deductibles lower your premium but increase what you pay out-of-pocket after a claim. Raising your deductible from $500 to $1,000 saves roughly $1,000 per year on Naples premiums, but this strategy only makes sense if you have liquid savings to cover that higher amount without financial hardship. Many families pick high deductibles to reduce monthly payments, then discover they cannot afford the deductible when a claim occurs. Choose a deductible you can actually afford to pay, because a lower premium means nothing if you cannot file a claim.

Flood and Wind Coverage Fill the Dangerous Gaps

Standard homeowners policies exclude flood damage entirely, which creates a catastrophic gap for Naples residents where hurricanes bring storm surge and heavy rainfall. You must purchase flood insurance separately through the National Flood Insurance Program or private insurers, and this decision cannot wait until a storm approaches. Tower Hill offers private flood endorsements up to $5 million, which provides an alternative to NFIP coverage with potentially better terms, while Security First and other carriers have different flood options. Your ZIP code determines your flood risk, and Naples shows dramatic variation in costs based on flood zone differences.

Windstorm coverage operates separately from standard policies as well, because wind damage from hurricanes exceeds what most homeowners policies cover. Many insurers require a separate windstorm endorsement or policy to protect against hurricane-force winds, making this a non-negotiable addition for coastal properties. Ask your agent directly whether your quote includes windstorm protection, because assuming it does without verification leaves you exposed to catastrophic loss.

Financial Strength and Claims Speed Determine Real Value

An insurer with low rates means nothing if they cannot pay claims after a hurricane, which is why AM Best financial ratings matter more than premium price alone. State Farm carries an AM Best A++ rating in Naples, Tower Hill holds a B rating, and Universal Property maintains an A rating, reflecting different levels of financial stability during crisis periods. Beyond ratings, customer complaint history reveals which insurers actually process claims efficiently or drag their feet during peak disaster periods. Shopping for the cheapest quote without checking financial ratings and complaint history is like buying a parachute on price alone-the savings disappear entirely when you need it to work.

Understanding what coverage you actually need sets the foundation for your next decision: how to find quotes that reflect your specific home and risk profile rather than generic estimates.

Getting Real Quotes That Match Your Home

Provide Identical Information to All Insurers

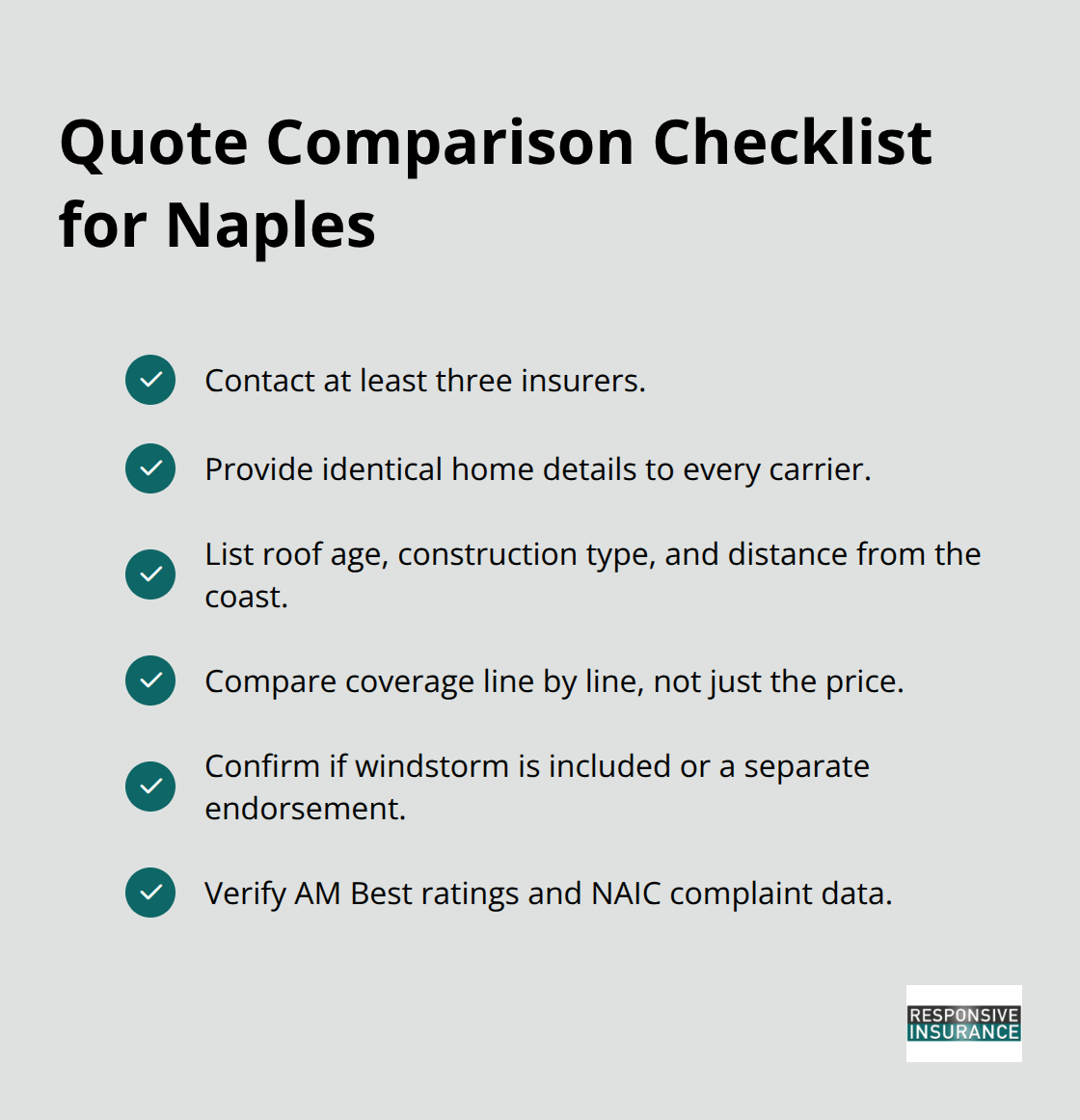

Start by contacting at least three different insurance providers and requesting quotes specific to your Naples property, not generic estimates based on ZIP code alone. When you call or visit websites, provide identical information across all quotes: your home’s age, square footage, construction type, roof condition, distance from coast, and any recent upgrades like impact-resistant windows or reinforced doors. This consistency matters because small differences in how you describe your home create wildly different premium estimates, and you cannot compare quotes fairly if one insurer thinks your roof is 15 years old while another assumes it’s 5 years old.

State Farm, Tower Hill, Universal Property, and Security First all operate in Naples, and each will quote you different prices for the same coverage. This difference exists not because one insurer is better, but because they price risk differently based on their underwriting models and claims experience.

Compare Coverage Details Line by Line

Once you have quotes in hand, compare them line by line by examining dwelling coverage limits, deductible amounts, flood endorsement options, and windstorm protection separately. A quote at $1,800 per year with only $300,000 in dwelling coverage is not cheaper than a $2,200 quote with $500,000 in coverage-you are buying fundamentally different products. Check whether each quote includes windstorm coverage or requires a separate endorsement, because this addition can cost $300–$600 annually in Naples and some insurers embed it while others list it separately.

Ask your agent directly whether the quote reflects replacement cost coverage (rebuilds without depreciation) or actual cash value (pays depreciated amounts), because this choice affects what you recover after a total loss. A quote with replacement cost coverage for a $500,000 dwelling is not the same as a quote with actual cash value and a $250,000 dwelling limit.

Verify Financial Strength and Claims History

Verify the financial strength rating for each insurer using AM Best ratings, and pull complaint data from the National Association of Insurance Commissioners to see how each company handles claims during high-volume periods like hurricane season. Tower Hill and Universal Property both operate in Naples, but Tower Hill recorded significantly higher complaint levels in 2022, which means you might pay less but face slower claims processing when you actually need it.

An insurer with low rates means nothing if they cannot pay claims after a hurricane, which is why AM Best financial ratings matter more than premium price alone. The premium difference shrinks dramatically once you account for what each policy actually covers, and the lowest number on paper often disappears when you examine the details. Contact a local agent to discuss your property’s specific needs and ensure your quotes reflect the actual protection available for your situation.

Final Thoughts

Finding the best homeowners insurance in Florida requires accepting one hard truth: the lowest premium rarely equals the best protection. Florida’s insurance market operates differently than the rest of the country because hurricane risk, limited carrier availability, and mandatory lender requirements have fundamentally changed what homeowners face. Naples residents pay 43% more than the national average, and that cost reflects genuine risk, not market inefficiency.

The comparison process matters because carriers price identical homes differently based on their underwriting models and claims experience. State Farm might quote $2,016 annually while Citizens charges $6,281 for the same dwelling coverage, and neither number is wrong-they reflect different business strategies and risk assessments. Tower Hill offers competitive base rates around $709 per year but carries higher complaint levels, while Universal Property balances affordability with private flood endorsements up to $5 million.

Contact multiple insurers with identical information about your home, compare coverage details line by line, and verify financial strength ratings before deciding. Do not assume windstorm coverage is included, do not choose a deductible you cannot afford, and do not skip flood insurance because your home is not in a designated flood zone. Reach out to our team to discuss your Naples home’s protection needs and find the best homeowners insurance in Florida that matches your situation.

![Hurricane Insurance Florida [Everything You Need to Know]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Hurricane-Insurance-Florida-_Everything-You-Need-to-Know__1769898428-80x80.jpeg)