Commercial Flood Insurance in Florida A Guide for Businesses

Florida businesses face significant flood risks from hurricanes, storm surge, and heavy rainfall. Standard commercial property insurance doesn’t cover flood damage, leaving many companies vulnerable.

We at Responsive Insurance, Inc. help Naples businesses understand their commercial flood insurance Florida options. This guide covers NFIP and private flood coverage to protect your business investment.

Why Florida Businesses Face Extreme Flood Risks

Hurricane Season Delivers Devastating Storm Surge

Florida businesses confront hurricane threats from June through November, with peak activity between August and October. The Gulf and Atlantic Coast faces storm surge risks that affect 6.4 million homes valued at $1.68 trillion according to recent data. Storm surge pushes water levels 15-20 feet above normal in coastal areas like Naples, which creates catastrophic floods that standard commercial property insurance won’t cover.

Hurricane wind risk impacts over 33 million homes in Gulf and Atlantic States, which represents $11.68 trillion in reconstruction costs. New York City leads in hurricane wind damage risk with 3.77 million homes at risk, but Florida businesses face the highest frequency of storm events throughout each season.

Sea Level Rise Accelerates Coastal Business Threats

Florida’s coastal elevation averages just six feet above sea level, which makes businesses extremely vulnerable to rising waters. Sea levels have risen eight inches since 1950 along Florida’s coast, with acceleration expected to reach 10-17 inches by 2040. Naples and Southwest Florida areas experience king tide floods during full moons even without storms present.

Coastal erosion removes 1-2 feet of beach annually in many areas, which pushes flood zones further inland and affects previously safe commercial properties. The National Flood Insurance Program updates flood maps regularly and often reclassifies low-risk properties into mandatory coverage zones.

Heavy Rainfall Creates Inland Flood Disasters

Florida receives 50-60 inches of rainfall annually (compared to the national average of 38 inches), with summer months delivering intense downpours that overwhelm drainage systems. Tropical storms and hurricanes dump 6-12 inches of rain in single events, which causes flash floods that can reach businesses miles from the coast.

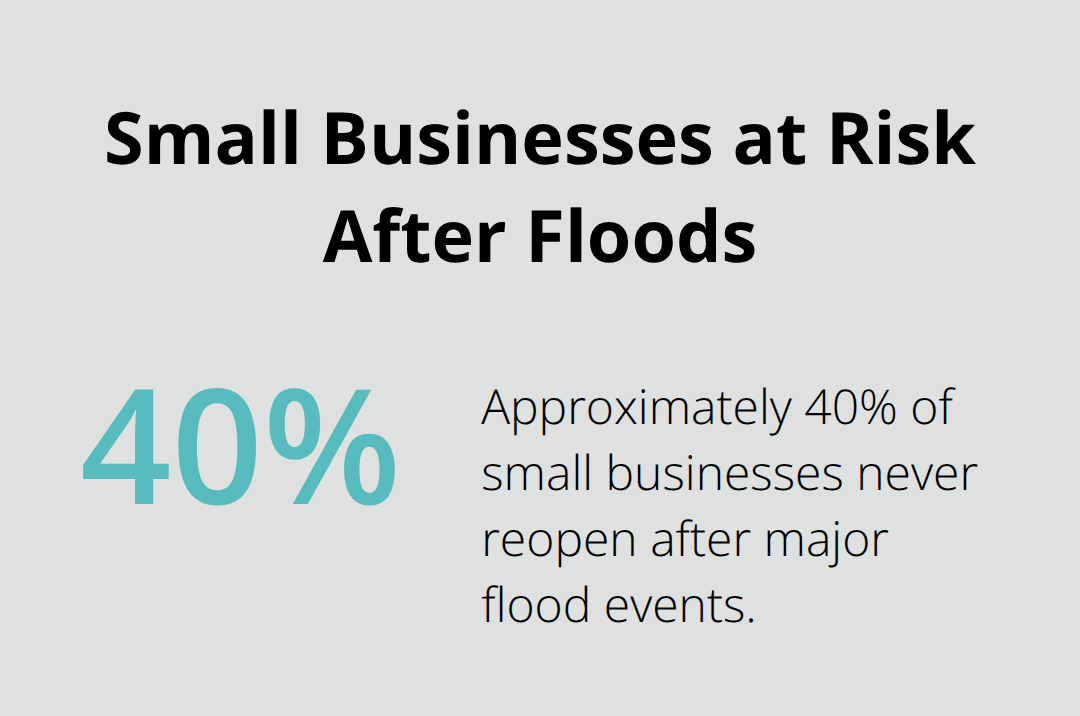

Urban development reduces natural water absorption, which forces more runoff into streets and commercial areas. Just one inch of water causes over $25,000 in damages to commercial properties, and approximately 40% of small businesses never reopen after major flood events.

These multiple flood threats make standard commercial property coverage inadequate for Florida businesses, which leads us to examine what protection gaps exist in traditional policies.

Understanding Commercial Flood Insurance Coverage

Standard commercial property insurance policies contain flood exclusions that leave Florida businesses exposed to catastrophic losses. These policies cover fire, theft, and wind damage but specifically exclude water damage from floods, storm surge, and surface water accumulation. The exclusion applies regardless of flood source – whether from hurricane storm surge, heavy rainfall, or overflowing drainage systems.

What Standard Commercial Property Policies Exclude

Commercial property policies exclude business interruption losses caused by flooding, which means companies cannot recover lost income during flood-related closures. Standard policies also exclude damage from mudflows, surface runoff, and water that backs up through sewers or drains. Even if wind damage creates an opening that allows flood water to enter, insurers will deny claims for water damage while only covering the initial wind damage.

The exclusions extend to equipment, inventory, and fixtures damaged by flood water. Businesses face total financial responsibility for cleanup costs, temporary relocation expenses, and lost revenue during repairs (which can stretch for months after major flood events).

NFIP Commercial Coverage Provides Basic Protection

The National Flood Insurance Program offers commercial flood insurance with building coverage up to $500,000 and contents coverage up to $500,000 per policy. NFIP policies operate on actual cash value basis, which reduces payouts due to depreciation calculations. The program includes Increased Cost of Compliance coverage up to $30,000 to help businesses meet updated building codes after flood damage.

NFIP policies require 30-day waiting periods before coverage becomes effective, which prevents last-minute purchases before storm threats. Businesses in Special Flood Hazard Areas with federally backed loans must purchase NFIP coverage under the Flood Disaster Protection Act. The average cost of NFIP flood insurance in Florida reaches $865 per year, though rates vary significantly by location and flood zone designation.

Private Flood Insurance Offers Superior Business Protection

Private flood insurance companies provide coverage limits that exceed NFIP’s $500,000 maximums, sometimes offering much more adequate coverage. Private policies may include/offer business interruption coverage (which NFIP excludes), allowing companies to recover lost income during flood repairs. These policies often use replacement cost coverage instead of actual cash value, which provides higher claim payments without depreciation deductions.

Private insurers often offer shorter waiting periods to activate coverage. Private market options become particularly valuable for businesses with high-value assets that exceed NFIP limits, though costs and requirements vary significantly between carriers and risk factors.

What Does Commercial Flood Insurance Cost in Florida

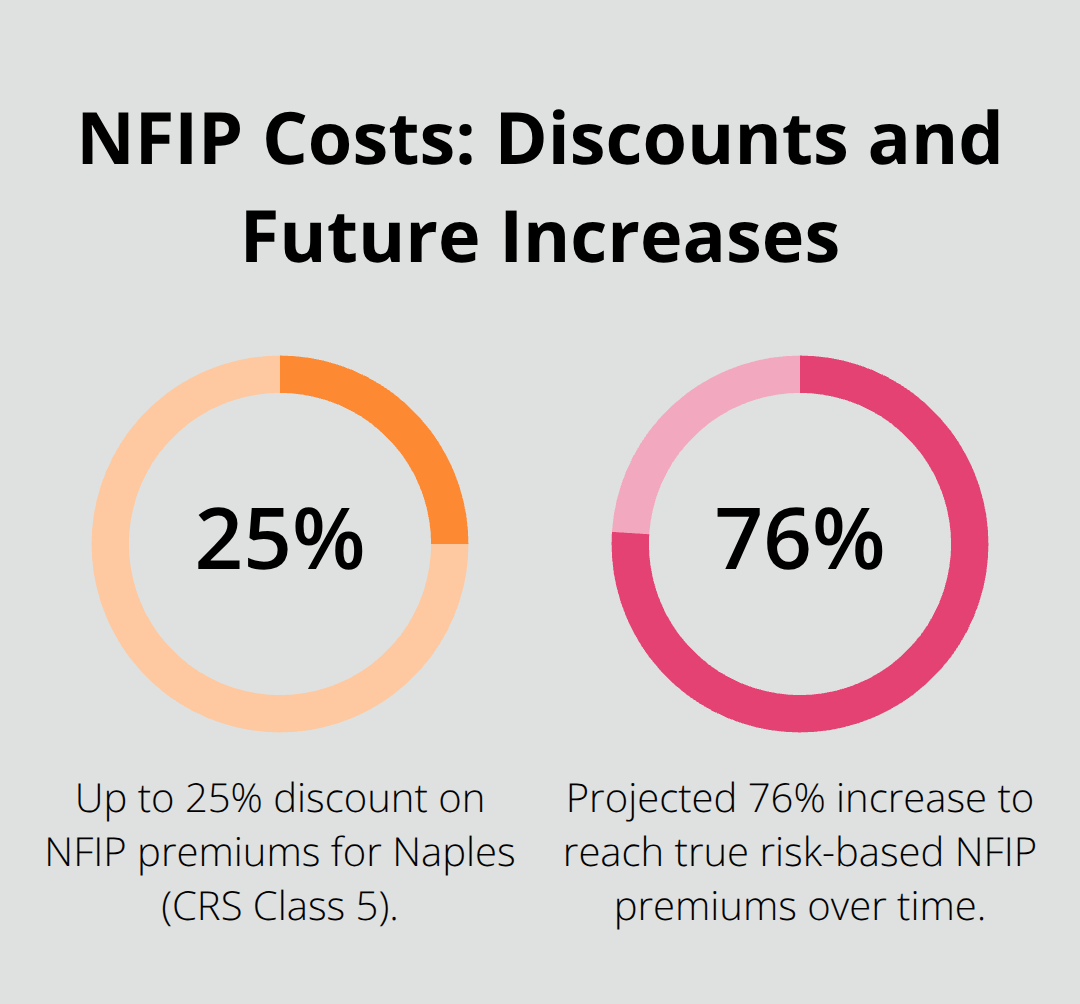

NFIP flood insurance costs vary dramatically across Florida based on flood zone classifications and Risk Rating 2.0 calculations. Properties in Zone AE face mandatory coverage requirements with average annual premiums of $865 statewide, though specific costs range from $483 in Bay County to $1,924 in Franklin County. Naples businesses benefit from the city’s Community Rating System Class 5 rating, which provides up to 25% discounts on NFIP premiums. The program’s Risk Rating 2.0 system now considers individual property characteristics rather than just flood zones, with the average Florida policyholder who paid $776 annually in 2023 while true risk-based premiums project at $1,363 (a 76% increase over time).

NFIP Rate Structure Limits Business Protection

NFIP commercial policies cap coverage at $500,000 for both structures and contents, which forces businesses with higher values to purchase multiple policies or seek private alternatives. The program uses actual cash value settlements that reduce payouts through depreciation calculations. The mandatory 30-day wait period when coverage isn’t part of a qualifying event like a loan closing prevents immediate coverage activation.

Businesses in Special Flood Hazard Areas with federally backed mortgages typically must purchase flood insurance. Properties outside special flood hazard areas, are still exposed to flooding risk but likely won’t be required by a lender to purchase flood insurance.

Private Market Offers Superior Coverage Options

Private flood insurers can offer effective dates with shorter wait periods and may provide replacement cost coverage options instead of depreciated actual cash value. These carriers frequently include a business interruption coverage option which is not available with the NFIP. This coverage allows companies to recover lost income due to not being able to operate their business during flood repairs. Private insurers can exceed NFIP’s $500,000 limits.

Premium costs vary significantly based on property elevation, construction details/costs, and proximity to water sources. Florida businesses with assets that exceed NFIP limits or that want broader coverage, should consider private coverage to avoid severe underinsurance gaps that could force permanent closure after major flood events.

Zone Classifications Drive Premium Calculations

Zone AE properties are one of the more common special flood hazard area zones. A special flood hazard area is an area that is considered to have at least a 1% annual flood chance designation. Zone VE coastal areas with wave action potential are considered an even higher exposure.

FEMA updates flood maps regularly, which can reclassify properties into a Special Flood Hazard Area when they weren’t previously in a SFHA, and visa versa. These changes can trigger mandatory coverage requirements for commercial property owners with loans on their property.

Final Thoughts

Commercial flood insurance can help businesses avoid closure after major flood events. Business interruption coverage, when available, can provide income during repairs and private flood insurance options often eliminate the NFIP’s $500,000 limits and potentially shorten the waiting period versus the NFIP 30 day wait when not part of a loan closing/qualifying event.

Florida business owners should evaluate their flood zone status immediately and obtain elevation certificates, which are no longer required but can reduce premiums. Properties outside Special Flood Hazard Areas still face significant risk (with 25% of flood claims occurring in these zones). The state’s 50-60 inches of annual rainfall and accelerating sea level rise make flood protection an essential consideration regardless of coastal proximity.

We at Responsive Insurance, Inc. work with private flood insurers and the NFIP for Naples businesses. Our independent agency structure allows us to find coverage that matches your specific property values and risk factors. Contact us today to protect your business investment from Florida’s flood threats.

![Home Insurance for Older Homes in Florida [What to Know]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Home-Insurance-for-Older-Homes-in-Florida-_What-to-Know__1766268849-80x80.jpeg)